Are you searching for a reliable family medical insurance quote? You are not alone. Millions of families every year struggle to find health coverage that is both comprehensive and affordable. This guide will help you understand how to get the best family medical insurance quote, compare plans smartly, and protect your loved ones without breaking your budget.

What Is a Family Medical Insurance Quote?

A family medical insurance quote is a personalized estimate of how much you will pay for a health insurance plan that covers every member of your household. This includes your spouse, children, and sometimes dependent parents.

When insurers calculate your family medical insurance quote, they look at:

- Ages of all covered family members

- Your zip code and state regulations

- Tobacco use history

- Chosen deductible level

- Type of plan (HMO, PPO, EPO, HDHP)

Getting at least three to five quotes side by side gives you the clearest picture of what the market offers for your specific situation.

Why Every Family Needs a Medical Insurance Quote

Skipping health insurance is a dangerous gamble. According to the Kaiser Family Foundation (dofollow), the average cost of a three-day hospital stay in the United States exceeds $30,000. A single emergency without coverage can devastate a family financially.

A proper family medical insurance quote helps you:

- Budget your monthly healthcare costs predictably

- Access preventive care before small issues become big problems

- Protect your savings from unexpected medical bills

- Qualify for tax benefits and government subsidies

How to Get an Accurate Family Medical Insurance Quote

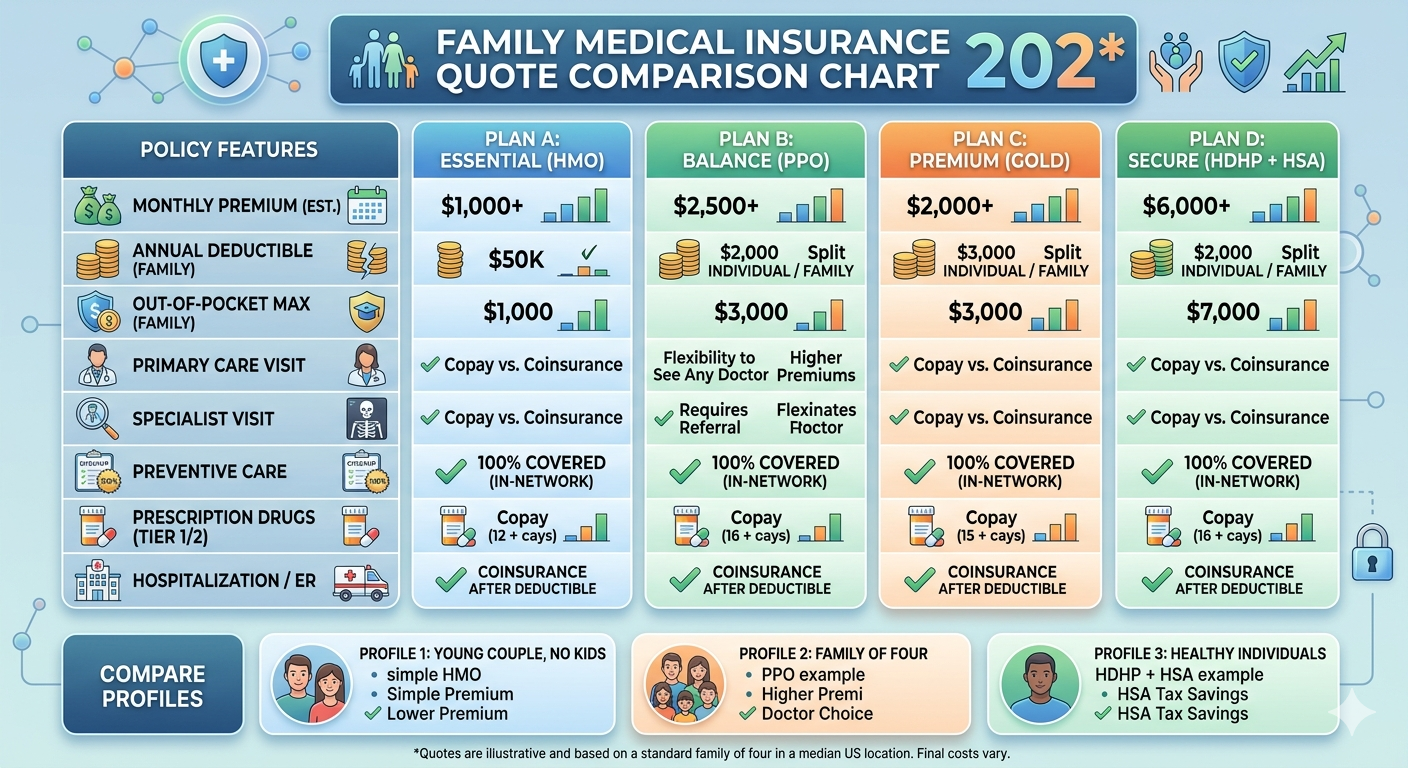

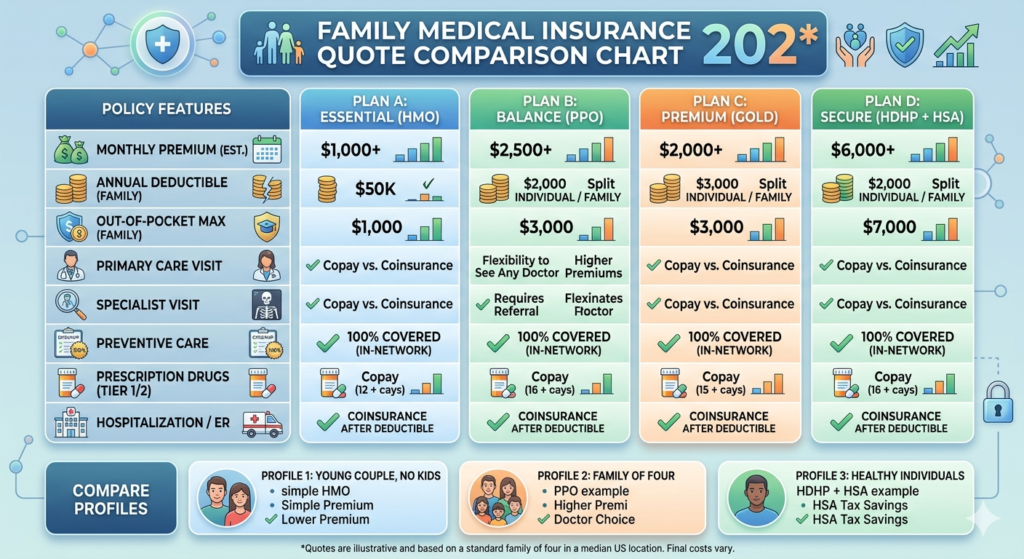

Show Image Alt text: family medical insurance quote comparison chart 2025

Follow these steps to get the most accurate family medical insurance quote possible:

Step 1 — Gather Your Family’s Information

Before requesting a quote, have ready the full names, dates of birth, and any pre-existing conditions for every family member you want covered.

Step 2 — Choose Your Coverage Level

Plans are generally categorized as Bronze, Silver, Gold, and Platinum. Bronze plans carry the lowest premiums but the highest out-of-pocket costs. Platinum plans are the opposite.

Step 3 — Compare Multiple Providers

Never rely on a single insurer. Use trusted comparison tools like HealthCare.gov (dofollow) to view multiple family medical insurance quote options in one place.

Step 4 — Check the Provider Network

Confirm that your preferred doctors, pediatricians, and nearby hospitals are included in the plan’s network before accepting any family medical insurance quote.

Step 5 — Review Prescription Drug Coverage

If any family member takes regular medications, verify that your chosen plan covers those specific drugs at an affordable co-pay.

Types of Family Medical Insurance Plans

Understanding plan types is essential before you accept any family medical insurance quote:

HMO – Health Maintenance Organization Lower premiums, requires referrals, limited to a specific network of doctors. Best for families who prefer lower costs and have a regular primary care physician.

PPO – Preferred Provider Organization More flexibility to see any doctor without a referral. Slightly higher premium but wider network. Good for families who see multiple specialists.

HDHP – High Deductible Health Plan Lowest monthly premiums, paired best with a Health Savings Account (HSA). Ideal for healthy families who want the most affordable family medical insurance quote and rarely need medical care.

EPO – Exclusive Provider Organization No referrals needed but strictly limited to in-network providers. A middle ground between HMO and PPO.

Here is the fully expanded “Key Factors That Affect Your Family Medical Insurance Quote” section with many more detailed points:

Key Factors That Affect Your Family Medical Insurance Quote

Several variables directly impact the price of your family medical insurance quote. Understanding each one gives you the power to make smarter choices and potentially save hundreds of dollars every year.

1. Number of Dependents

Adding more family members to your plan increases the premium, though many insurers cap the child surcharge after three children. This means a fourth or fifth child may add very little — or nothing at all — to your family medical insurance quote. Always ask your insurer specifically about their dependent pricing structure before enrolling.

2. Geographic Location

Where you live has a major impact on your family medical insurance quote. States with more insurance competition — such as California, Texas, and Florida — tend to offer a wider range of lower-cost options. Rural areas typically have fewer providers in the network, less market competition, and as a result, significantly higher premiums. Even moving from one county to another within the same state can change your quote dramatically.

3. Deductible Amount

Choosing a higher deductible lowers your monthly premium and reduces the overall family medical insurance quote cost. For example, raising your deductible from $1,000 to $3,000 could cut your monthly premium by 20 to 30 percent. This trade-off works well for healthy families who rarely need medical care beyond routine checkups.

4. Tobacco Use

Insurers in most states are legally allowed to charge tobacco users up to 50 percent more on premiums compared to non-smokers. This surcharge applies to any adult on the plan who has used tobacco products within the last 12 months. Quitting tobacco is one of the fastest ways to reduce your family medical insurance quote at renewal time.

5. Plan Tier — Metal Level

The metal tier you choose has the single biggest impact on your monthly quote amount. Here is a quick breakdown:

- Bronze — Lowest premium, highest out-of-pocket costs. Covers roughly 60% of medical expenses.

- Silver — Moderate premium and cost-sharing. Covers roughly 70% of costs. Best for families who qualify for cost-sharing reductions.

- Gold — Higher premium, lower deductible. Covers roughly 80% of costs. Ideal for families who use healthcare frequently.

- Platinum — Highest premium, lowest out-of-pocket. Covers roughly 90% of costs. Best for families with chronic conditions or high medical needs.

Choosing the right tier is critical to getting the most value from your family medical insurance quote.

6. Ages of Family Members

Age is one of the most significant pricing factors in any family medical insurance quote. Older adults cost insurers more to cover, so their premiums are higher. In most markets, insurers can charge older adults up to three times more than younger enrollees for the same plan. Adding aging parents or in-laws to your plan will noticeably increase your overall quote.

7. Plan Type — HMO, PPO, EPO, HDHP

The structure of your plan directly affects your family medical insurance quote. HMOs are the most affordable but most restrictive. PPOs offer the most flexibility but come at a higher price. HDHPs carry the lowest premiums but require higher out-of-pocket spending before coverage kicks in. Choosing the wrong plan type for your family’s usage patterns means either overpaying monthly or facing unexpected bills when you need care.

8. Annual Household Income

Your income level determines whether you qualify for premium tax credits or government subsidies through the marketplace. Families earning between 100 and 400 percent of the federal poverty level are eligible for significant financial assistance that can reduce their family medical insurance quote by hundreds of dollars per month. Always check your subsidy eligibility before purchasing a private plan at full price.

9. Pre-Existing Medical Conditions

Under current law in the United States, insurers cannot deny coverage or charge higher premiums based on pre-existing conditions for marketplace plans. However, short-term health plans and some employer-sponsored plans may still factor medical history into your family medical insurance quote. Always confirm the plan type before assuming pre-existing conditions are fully covered.

10. Network Size and Quality

Plans with larger, broader provider networks typically cost more. A family medical insurance quote from a plan with access to major hospital systems, top-rated specialists, and nationwide coverage will naturally carry a higher premium than a plan limited to a small regional network. If your family travels frequently or lives between two locations, a wider network is worth the extra cost.

11. Coverage Add-Ons and Riders

Optional add-ons such as dental coverage, vision care, maternity riders, critical illness coverage, and mental health benefits all increase the total cost of your family medical insurance quote. However, many of these riders provide excellent value — especially dental and vision for families with children — when compared to paying out of pocket for those services.

12. Employer Contribution

If your health insurance is offered through your workplace, your employer typically covers a portion of the premium. The size of that contribution directly affects your net family medical insurance quote. Employers are required to cover at least 50 percent of the employee’s premium, but contributions toward dependents vary widely by company. Always calculate your true out-of-pocket cost after the employer contribution before comparing workplace plans to marketplace alternatives.

13. Claim History

While marketplace plans cannot use your medical history against you, some group plans and short-term health plans do consider your family’s past claims history when calculating your family medical insurance quote. Families with a history of frequent or high-cost claims may face higher renewal premiums on certain plan types.

14. Waiting Periods

Some plans — particularly those offered outside the standard marketplace — include waiting periods for certain treatments, surgeries, or pre-existing conditions. A plan with a 12-month waiting period on maternity care, for example, may appear cheaper on your family medical insurance quote but could cost you far more if you need that coverage soon after enrolling.

15. Coinsurance Percentage

After you meet your deductible, coinsurance determines how costs are split between you and your insurer. A plan with an 80/20 coinsurance split means the insurer pays 80 percent and you pay 20 percent of all covered costs until you hit your out-of-pocket maximum. Plans with a higher insurer share — such as 90/10 — typically carry a higher monthly premium in your family medical insurance quote but offer greater financial protection for high-cost medical events.

16. Out-of-Pocket Maximum

Every plan has a cap on the total amount you will pay in a single plan year. Once you reach this maximum, the insurer covers 100 percent of all remaining covered costs. Plans with a lower out-of-pocket maximum are more protective but usually result in a higher family medical insurance quote. For families with members managing serious illnesses or frequent medical needs, a lower out-of-pocket maximum is well worth the higher premium.

17. HSA Eligibility

Plans that are HSA-compatible — typically HDHPs — allow you to contribute pre-tax dollars to a Health Savings Account. This effectively reduces the true cost of your family medical insurance quote because every dollar you contribute to an HSA is shielded from federal income tax. For families in higher tax brackets, this benefit alone can save thousands of dollars annually.

18. Open Enrollment Timing

When you enroll also matters. Missing the standard open enrollment window means you can only sign up during a Special Enrollment Period triggered by a qualifying life event such as marriage, childbirth, or job loss. Enrolling outside of these windows is generally not possible, and gaps in coverage can affect the pricing and terms of your next family medical insurance quote.

19. State-Specific Regulations

Each state has its own rules governing what insurers must cover, how much they can charge, and what protections families are entitled to. States like New York and Massachusetts have stricter consumer protections, which can result in more standardized — and sometimes higher — quotes. States with fewer regulations may offer more plan variety but less guaranteed protection in your family medical insurance quote.

20. Insurer’s Administrative and Profit Margin

Finally, not all insurers operate with the same efficiency. Some pass higher administrative costs and profit margins on to customers in the form of higher premiums. Under the Affordable Care Act, insurers are required to spend at least 80 percent of premium revenue on actual medical care — known as the Medical Loss Ratio rule. Choosing an insurer with a strong MLR track record ensures more of your premium dollar goes toward your family’s health rather than corporate overhead.

How to Lower Your Family Medical Insurance Quote

Here are practical strategies to reduce the cost of your family medical insurance quote without sacrificing essential coverage:

- Apply for subsidies — Visit HealthCare.gov (dofollow) to check if your household qualifies for premium tax credits based on your income level

- Open an HSA — A Health Savings Account lets you pay medical costs with pre-tax dollars, effectively reducing your real-world costs

- Stay in-network — Always using in-network providers prevents costly surprise bills

- Use telemedicine — Many plans include free or low-cost virtual visits, reducing your need for expensive in-person appointments

- Review annually — Plans and pricing change every year, so always get a fresh family medical insurance quote during open enrollment

Family Medical Insurance Quote vs Individual Plans

Many families wonder whether one family plan or multiple individual plans makes more financial sense. In almost every case, a single family medical insurance quote covering all members is more cost-effective than separate individual policies.

Family plans benefit from:

- One combined deductible and out-of-pocket maximum

- Simpler administration with a single insurer

- Often lower per-person costs at higher family sizes

According to eHealth Insurance (dofollow), families who bundle coverage under one plan save an average of 20 to 30 percent compared to purchasing individual policies separately.

Read More on wetou.fun

Before you make a final decision on your plan, explore these related guides on our website:

- 👉 Most Affordable Family Health Insurance Plans

- 👉 Family Medical Coverage Explained

- 👉 Medical Insurance Policy for Family: What to Look For

- 👉 Get a Free Insurance Quote Today

External Resources Worth Reading

These trusted external sources will help deepen your understanding:

- 🔗 Kaiser Family Foundation – Health Insurance Explainer (dofollow)

- 🔗 HealthCare.gov – Compare Plans & Prices (dofollow)

- 🔗 eHealth – Family Health Insurance Guide (dofollow)

- 🔗 CDC – Importance of Health Coverage (dofollow)

Final Thoughts: Get Your Family Medical Insurance Quote Today

Your family’s health is priceless, but that does not mean your insurance has to be unaffordable. Getting a family medical insurance quote is the first and most important step toward securing reliable, long-term protection for everyone you love.

Compare plans, check subsidies, review the network, and revisit your coverage every year. The right family medical insurance quote is out there — and with the right information, you will find it.

Ready to get started? Use our free comparison tool at wetou.fun and receive your personalized family medical insurance quote in minutes.