Term Life vs Whole Life Insurance: 5 Biggest Differences You Must Know

Table of Contents

Term Life vs Whole Life Insurance: What Every Family Needs to Know in 2026 {#what-is}

Term life vs whole life insurance — it’s one of the most important financial decisions your family will ever make, yet most people find it completely confusing.

Here’s the honest truth: choosing the wrong type of life insurance could cost you tens of thousands of pounds over your lifetime. And most people never realise it until it’s too late.

In this guide, we break down the 5 biggest differences between term life and whole life insurance in plain English — no jargon, no fluff — so you can make the right call for your family today.

According to Investopedia, term life insurance is the right choice for the majority of families, yet millions of people end up paying far more than they need to for whole life policies they don’t fully understand. The Insurance Information Institute also confirms that term life remains the most purchased type of individual life insurance globally.

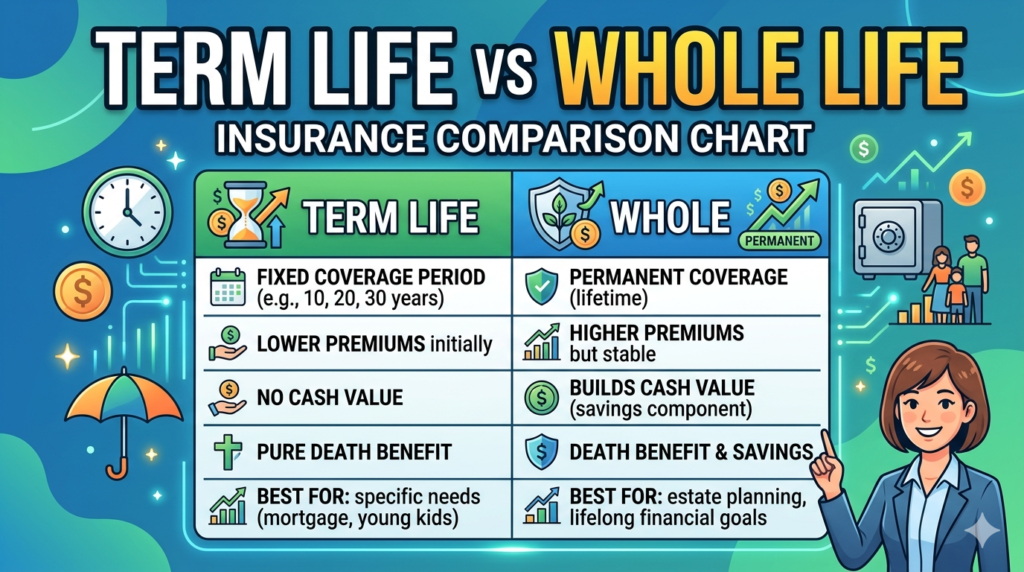

What Is Term Life Insurance? {#term-life}

Term life insurance is the simpler, more affordable option in the term life vs whole life insurance debate. Here’s how it works:

You choose a fixed period — typically 10, 20, or 30 years — and pay a set monthly premium throughout. If you pass away during that period, your family receives the death benefit payout. If you outlive the policy, it expires with no payout and no penalty.

Alt text: term life vs whole life insurance comparison chart showing how term life works over 20 years

Alt text: term life vs whole life insurance comparison chart showing how term life works over 20 years

Key Features of Term Life Insurance

- Lower premiums — typically 5–10x cheaper than whole life for the same coverage

- Simple and transparent — pure protection with no hidden investment components

- Flexible term lengths — 10, 15, 20, or 30 years to match your needs

- No cash value — you pay for protection only, which keeps costs low

- Renewable — many policies allow renewal at the end of the term (at a higher rate)

Who Is Term Life Insurance Best For?

Term life insurance is the right choice for:

- Young families with children under 18

- Homeowners with a mortgage to protect

- People on a tight budget who need maximum coverage

- Anyone who wants simple, no-fuss life protection

- People in their 20s, 30s, or early 40s just starting out

Real example: A healthy 30-year-old non-smoker can get £500,000 of term life cover for roughly £15–£25 per month on a 20-year policy. That’s less than a monthly streaming subscription — for half a million pounds of family protection.

What Is Whole Life Insurance? {#whole-life}

Whole life insurance is a permanent policy that covers you for your entire life, not just a fixed period. As long as you keep paying premiums, the policy never expires.

Unlike term life, whole life insurance builds cash value over time. A portion of each premium goes into a savings-like account that grows slowly on a tax-deferred basis. You can borrow against this cash value or withdraw it while you’re still alive.

Key Features of Whole Life Insurance

- Lifelong coverage — never expires, no matter how old you get

- Cash value accumulation — grows tax-deferred over time

- Guaranteed death benefit — your beneficiaries will definitely receive a payout

- Higher premiums — typically 5–15x more expensive than term life

- Policy loans — you can borrow against the cash value if needed

Who Is Whole Life Insurance Best For?

Whole life is not the right choice for most people, but it genuinely suits:

- High earners who have already maxed out pensions and ISAs

- People with lifelong dependants (such as a disabled family member)

- Business owners using insurance for succession planning

- Those with large estates who want to offset inheritance tax

- Anyone who wants a guaranteed payout regardless of when they die

Term Life vs Whole Life Insurance: 5 Key Differences {#comparison}

Here are the 5 most important differences between term life vs whole life insurance:

1. Cost

This is the biggest difference. Term life insurance is dramatically cheaper. For the same £500,000 death benefit, a healthy 35-year-old might pay:

- Term life: £20–£30/month

- Whole life: £200–£400/month

That’s up to 15x more expensive for whole life — and the extra cost doesn’t always translate to better value for most families.

2. Duration

- Term life: Covers a fixed period (10–30 years). When the term ends, cover stops.

- Whole life: Covers you for your entire lifetime, no matter when you die.

3. Cash Value

- Term life: No cash value. Your premiums buy pure protection.

- Whole life: Builds cash value over time that you can access while alive.

4. Payout Guarantee

- Term life: Only pays out if you die within the policy term.

- Whole life: Guaranteed to pay out, since it covers your whole life.

5. Complexity

- Term life: Extremely simple. Fixed premium, fixed term, fixed payout.

- Whole life: More complex. Involves investment elements, surrender charges, and policy loans.

Full Comparison Table

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage period | Fixed (10–30 years) | Lifetime |

| Monthly premium | Low (£15–£50/mo) | High (£100–£400/mo) |

| Cash value | No | Yes, grows over time |

| Payout guaranteed? | Only if you die in term | Yes, always |

| Best for | Families, mortgage holders | High earners, estate planning |

| Complexity | Simple | More complex |

| Investment element | No | Yes (modest returns) |

| Typical CPC (ad value) | High | High |

Is Term Life Insurance Worth It? {#is-term-worth-it}

Yes — for the vast majority of people, term life insurance is absolutely worth it and is almost always the smarter financial choice when comparing term life vs whole life insurance.

Here is why financial experts consistently recommend term over whole life:

Reason 1: The “Buy Term and Invest the Difference” Strategy Wins

The premium difference between term and whole life is typically £150–£300/month. If you invest that difference in a simple index fund earning an average of 7% annually, you will almost certainly end up with far more wealth than the cash value accumulated inside a whole life policy — which typically grows at just 1–3.5% per year.

According to Forbes, this strategy is recommended by most independent financial advisers for families who are not high earners.

Reason 2: Your Need for Insurance Decreases Over Time

When your children grow up, your mortgage is paid off, and your retirement pot is built, you simply don’t need the same level of life cover. A term policy that aligns with your financial obligations and then expires is perfectly logical — and efficient.

Reason 3: Whole Life Returns Are Modest

The cash value inside a whole life policy typically grows at 1–3.5% annually. Compare that to a global index tracker which has historically returned 7–10% annually over long periods. For wealth building, whole life is rarely the best tool.

Which Type of Life Insurance Should You Choose? {#which-one}

When deciding between term life vs whole life insurance, ask yourself these 3 questions:

Question 1: Do I have dependants who rely on my income?

- Yes → You need life insurance. Start with term life.

- No → Life cover may not be urgent right now.

Question 2: What is my budget for premiums?

- Limited budget → Term life is the only practical choice. Get covered first.

- High income with maxed-out investments → Whole life may be worth exploring.

Question 3: How long do I need coverage?

- Until kids are grown / mortgage is paid off → Term life, matched to that timeframe

- For my entire life, no matter when I die → Whole life

Our recommendation: If you are in your 20s, 30s, or 40s with a family and a mortgage, term life insurance is almost certainly the right choice. Get a 20 or 25-year policy that covers your peak financial obligations.

How to Get the Cheapest Life Insurance Policy in 2026 {#cheapest}

Getting the best rate on a cheapest life insurance policy comes down to a few proven factors:

- Buy young and healthy — your health at application locks in your rate for the entire term

- Choose term over whole life — instantly reduces premiums by 70–90%

- Quit smoking — smokers pay up to double the premium of non-smokers

- Maintain a healthy BMI and blood pressure — insurers base pricing on health risk

- Choose the right term length — match it to your mortgage or until your youngest child turns 21

- Compare at least 3 quotes — premiums vary significantly between insurers for identical cover

- Apply sooner rather than later — every year you wait increases your premium

For best life insurance for families, look for policies that offer critical illness cover as an add-on — it can protect you if you’re diagnosed with a serious condition and unable to work, not just if you die.

Common Mistakes to Avoid When Choosing Life Insurance {#mistakes}

Waiting too long. A 30-year-old pays significantly less than a 45-year-old for identical coverage. The best time to buy life insurance is today.

Underestimating how much cover you need. A common rule of thumb: 10–12x your annual income. Earning £35,000? Aim for at least £350,000–£420,000 in coverage.

Choosing whole life when you can’t sustain the premiums. Research shows that millions of whole life policies are cancelled within the first 10 years because the premiums become unaffordable — and policyholders lose most of what they paid in. A term policy you can maintain beats an expensive policy you eventually drop.

Confusing term life vs whole life insurance as the same product. They serve very different purposes. Understand what you’re buying before signing.

Not naming a beneficiary. Without a named beneficiary, your payout could get tied up in probate for months — leaving your family without funds when they need them most.

Frequently Asked Questions About Term Life vs Whole Life Insurance {#faqs}

Can I have both term and whole life insurance? Yes. Some people hold a term policy for primary income protection and a smaller whole life policy for estate planning or final expenses. This is sometimes called a “laddering” strategy.

What is whole life insurance used for if term is cheaper? Whole life insurance is primarily used for permanent needs: covering final expenses at any age, business succession planning, or high-net-worth estate planning where a guaranteed lifelong payout is essential.

What happens to term life insurance if I outlive the policy? The policy simply ends with no payout. Some term policies are “convertible,” allowing you to switch to a whole life policy without a new medical exam. Others offer a “return of premium” rider, though this significantly increases cost.

Can I get life insurance for 30s with no medical exam? Yes — many insurers now offer simplified underwriting or “no exam” policies, especially for younger, healthier applicants seeking lower coverage amounts. However, these policies typically cost slightly more than fully underwritten ones.

How do I get term life insurance quotes today? You can get term life insurance quotes online through comparison sites or directly from insurers. Most require basic details: your age, health status, coverage amount, and desired term length. Always compare at least 3 providers before deciding.

Is whole life insurance a good investment? Generally, no — not for most people. The returns on the cash value component (1–3.5% annually) are well below what you’d earn investing the premium difference in a diversified portfolio. Whole life has specific use cases, but “investment” for the average family isn’t typically one of them.

Final Verdict: Term Life vs Whole Life Insurance

When it comes to term life vs whole life insurance, the winner for the majority of families is clear: term life insurance.

It delivers maximum protection at minimum cost, during the exact years your family needs it most. It’s simple, affordable, and purpose-built for real-life financial obligations like mortgages, childcare, and income replacement.

Whole life has its place — but only for a small subset of high earners and estate planners with very specific needs.

The most important thing? Don’t wait. Every year you delay is a year your family goes unprotected — and a year older you’ll be when you finally do apply.

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Always consult a qualified financial adviser before purchasing any insurance product. External links are provided for reference and education only.